Welcome to the “Election Year” column. As the global geopolitical economic landscape becomes increasingly polarized, this column will focus on election events that have a significant impact on markets, business and policy.

Japan’s election on Sunday was a near disaster for the ruling party, which has been in power for almost all of its history since its founding in 1955, but failed to win a majority of seats, its first defeat since 2009. The defeat was largely due to a corruption scandal involving officials who hid donations and used the funds for personal use, which touched a nerve among voters at a time of growing economic pressure.

In order to form a government, the LDP has had to seek cooperation with other parties, a rare situation for the LDP. The good news is that although the opposition has strengthened, it is still divided and unable to form an effective coalition.

Regardless of who ultimately forms the government, there will be no significant changes in policy. Japan has a consensus on many issues, especially its alliance with the United States. The opposition may push for accountability for U.S. troops stationed in Japan, but due to the growing threats from China and North Korea, Japan’s relationship with the United States will not change significantly in the short term.

Market investors will focus on whether the Bank of Japan’s policy will change. The main opposition party proposed to change the inflation target of 2% to “above zero”, which, if passed, may mean a tightening of policy. However, it is not easy to gain broad party support. In recent years, the increase in prices has hit a record high in decades.

For investors, the bigger concern is the future of Prime Minister Shigeru Ishiba, who took office on Oct. 1 promising to stay in power, but the election results have made his position more vulnerable. If the LDP stays in power, a likely successor would be Sanae Takaichi, who narrowly lost to Ishiba in an internal party election last month.

Japan is at a point where international military and trade tensions are rising, and a weak government may face greater challenges. It is worth noting that former US President Trump may return to the White House, which will put Japan under more pressure in the future.

For the Japanese people, electing politicians they can trust is a top priority, but whether this wish will be realized remains to be seen.

Japanese Economy Q&A

Bloomberg economist Taro Kimura discusses the impact of the election results on the Japanese economy.

At present, no matter who comes to power, Japan may face a weaker government. What impact will this have on the policy of the Bank of Japan?

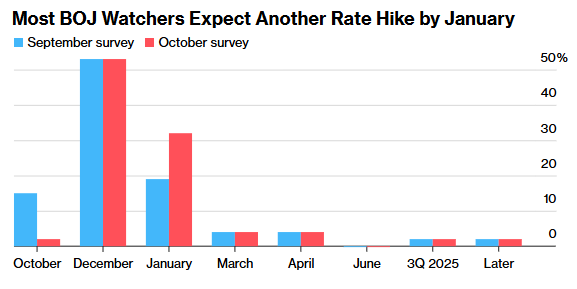

The Bank of Japan may face political pressure to stop raising interest rates this year as rising debt costs are unattractive to voters. Prime Minister Shigeru Ishiba may hope to form a coalition government with key opposition parties – the Democratic Party for the People and the Japan Restoration Party – whose policies focus on helping struggling households and small and medium-sized enterprises and are not expected to easily support rate hikes.

Still, lawmakers are unlikely to delay the central bank’s tightening policy for long. Japan’s inflation has been above 2% for two years and is still rising, driven by rising wages and a weak yen. Opposition lawmakers may call on the Bank of Japan to raise interest rates once the situation stabilizes to counter rising living costs.

Shigeru Ishiba, known for criticizing former Prime Minister Shinzo Abe’s economic policies, favors normalizing fiscal policy and stabilizing Japan’s huge debt burden, but he may put this issue aside for now. He is expected to increase fiscal support for low-income households, and the opposition party also advocates tax cuts in its election manifesto to ease people’s living pressures. This policy will help promote growth in the short term, but it may also push up inflation and further increase Japan’s public debt burden.

What are the main challenges facing the next government?

Clearly, Ishiba’s road to power is fraught with difficulties. He needs to win support by forming a minority government or expanding the coalition. The last time the LDP faced such a complex situation was in the early 1990s. The recent fundraising scandal and the cost of living crisis due to high inflation show no signs of dissipating in the short term. Sunday’s election marks the beginning of an unprecedented period of highly uncertain politics in Japan.

Market reaction

Veteran Asian equities reporter Hideyuki Sano discusses the market’s reaction to the LDP’s setback.

Investors have almost assumed that Japan’s political situation is stable since late 2012, with the Liberal Democratic Party and its ruling coalition partner, Komeito, maintaining a majority. However, the poor performance in the election has challenged that assumption.

Many analysts believe the political deadlock could keep investors on the sidelines regarding Japanese assets, weighing on the yen and Japanese stocks.

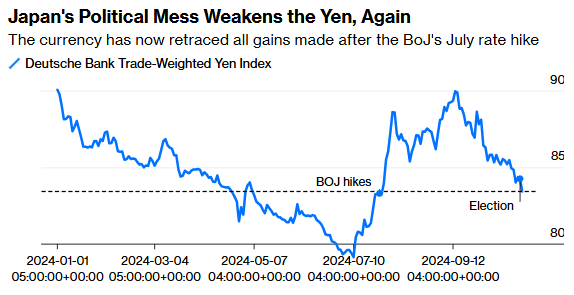

Yen weakens again

The yen strengthened after the Bank of Japan raised interest rates in July, but has now given up all of its gains.

Investors expect Ishiba to eventually reach a deal with the smaller conservative Democratic Party for the People, as the LDP has done in the past when it lost its majority. However, with Ishiba’s leadership weakened after the election, markets are skeptical about his ability to effectively boost Japan’s economic growth.

The yen is particularly vulnerable. Ishiba’s potential coalition partners, the Democratic Party for the People and the Japan Restoration Party, support loose monetary policy, suggesting the Bank of Japan may face pressure to raise interest rates further. In addition, some market participants are concerned that Ishiba may increase fiscal spending to attract voters, especially with the upper house election approaching next year, which could further worsen Japan’s already weak fiscal position.

Corporate Impact

Tokyo journalist Nicholas Takahashi believes the outlook for Japanese companies is changing.

The LDP government has for years urged Japan’s largest companies to reduce cross-shareholdings to improve governance and promote competition, and earlier this year Toyota Motor Corp. planned to buy back 1.2 trillion yen of strategic shares, a sign that the reform is starting to make progress.

However, 7&I Holdings’s request for government protection as it tries to fend off a takeover by Couch-Tard shows that plans to attract foreign investment are not all smooth sailing.

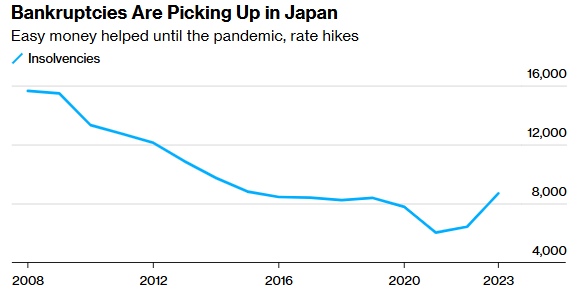

At the same time, a series of regulatory scandals have cast a shadow over Japan’s auto industry, while the Bank of Japan’s move to end its ultra-loose monetary policy has put countless companies on the verge of bankruptcy under greater pressure.

With the LDP’s important role shaken, Japan’s business community may face a more complex environment and it will be more difficult to navigate in the future.